You're sitting there, looking at your screen, and you see it. 744. It’s a weirdly specific number, isn't it? It feels high, but it’s not that mythical 800 or 850 that people brag about on LinkedIn or at boring dinner parties. Honestly, having a credit score of 744 puts you in a bit of a sweet spot, but there’s a lot of nuance that the big banks don’t always spell out for you.

It’s Very Good. That’s the official FICO label.

But labels are kinda useless when you're trying to buy a house in a market that's moving at 100 miles per hour. According to data from FICO, a score of 744 is well above the national average, which usually hovers around the 715 to 718 mark depending on the quarter. You’ve basically outpaced about 60% of the American population. That feels great, right? It should. But if you think a 744 makes you invincible to a rejection letter, you might want to slow down just a second because lenders look at more than just that three-digit number.

What a credit score of 744 actually buys you in today's market

Let’s talk turkey. Or money. Whatever you want to call it.

When you walk into a dealership or apply for a mortgage with a credit score of 744, you are generally walking into "Tier 1" territory. Most lenders have these invisible buckets. If you’re in the top bucket, you get the lowest interest rates. Usually, that cutoff is 740. You made it by four points. Those four points could literally save you tens of thousands of dollars over a 30-year mortgage compared to someone sitting at a 735. It’s a thin line, but the financial implications are massive.

Take an auto loan, for example. If you’re looking at a $40,000 truck, a 744 score might snag you an APR of 5.5%, while a "Fair" score might leave you crying at 12%. Over five years, that's a difference of thousands in interest alone. You're basically getting a discount on life just for being responsible.

But here’s the kicker. Even with a 744, a lender might still turn you down if your Debt-to-Income (DTI) ratio is trash. You could have a perfect payment history, but if you’re trying to buy a mansion on a barista’s salary, that 744 isn't going to save you. Lenders like Chase or Wells Fargo are looking for a story, not just a number. They want to see that you've handled different types of credit—like a mix of credit cards and maybe an old student loan—without breaking a sweat.

The psychology of the 740-750 range

It’s a funny place to be. You’re so close to the "Exceptional" 800+ club that you can almost taste it. Most people at 744 are there because they do everything right but maybe their "credit age" is a bit young. Or perhaps they have one credit card that’s slightly too close to its limit.

I’ve seen people obsess over moving from 744 to 760. Does it matter? Honestly, not really. In the eyes of a mortgage broker, 744 and 760 are often treated as the exact same thing. You’re already getting the "best available rate." Chasing those extra points is sometimes just a hobby for people who like spreadsheets. If you have a 744, you've already won the game of "not paying extra for money."

Why your score might be stuck at 744

If you've been hovering at this number for months, you’re probably wondering why it won't budge. Credit scoring models, especially FICO 8 (which is what most lenders use), are sensitive to small things.

Maybe you have a $10,000 limit on a card and you’re carrying a $2,900 balance. That’s 29% utilization. It’s "fine," but the "excellent" crowd usually stays under 10%. Just paying that down to $900 could pop you into the 760s overnight.

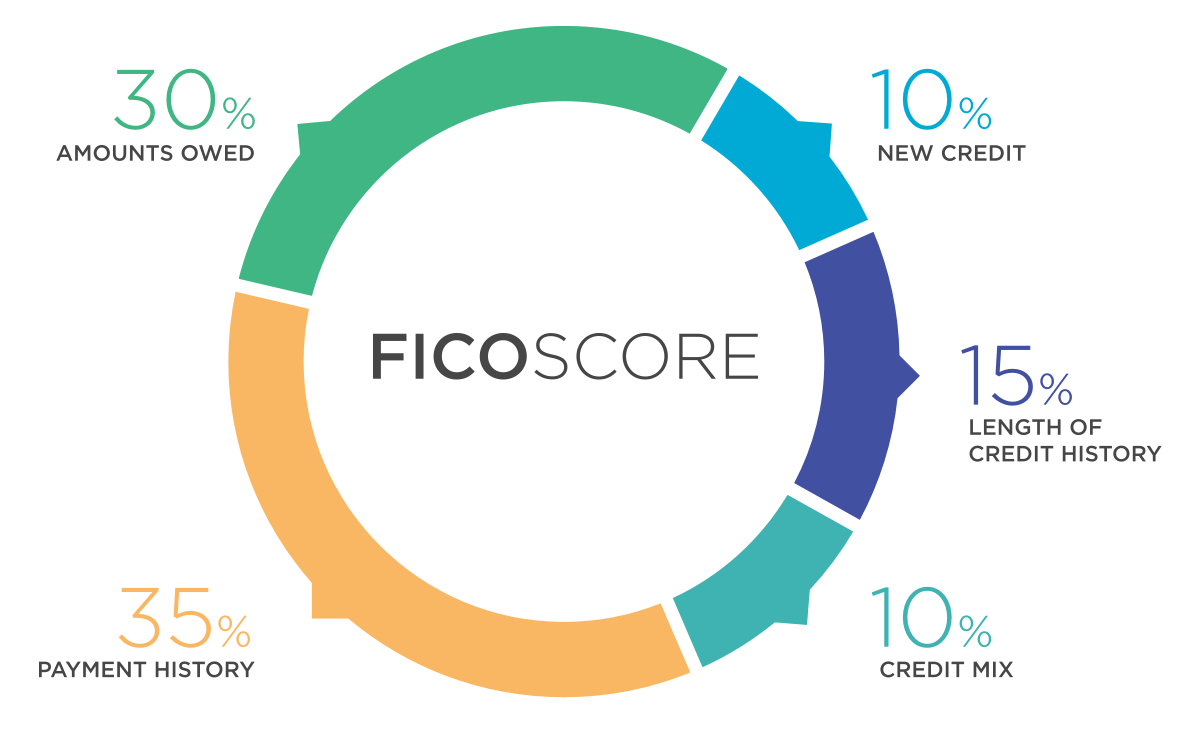

Then there’s the "Credit Mix" factor. If you only have credit cards and no "installment loans" (like a car loan or a mortgage), your score might plateau. The algorithm likes to see that you can handle different rhythms of repayment. Credit cards are "revolving"—you choose how much to pay. Mortgages are "installment"—you pay the same amount every month. Being good at both is what sends your score into the stratosphere.

- Payment History: You probably haven't missed a payment in years.

- Credit Utilization: This is likely where your 744 is being "held back."

- Length of Credit History: You can't rush time. If your oldest account is only 5 years old, you're just waiting for the clock to tick.

- New Credit: Did you just apply for a New Visa? That hard inquiry probably knocked you down a few points.

Real world impact: Mortgage vs. Credit Cards

Let's look at a real scenario. Say you’re looking at a $500,000 home.

With a credit score of 744, you are likely qualifying for the Prime rate. According to the Freddie Mac Primary Mortgage Market Survey, even a 0.5% difference in your interest rate can change your monthly payment by hundreds of dollars. Over 30 years? That's the price of a luxury car in interest savings.

On the credit card side, a 744 is a golden ticket. You can pretty much apply for the "heavy hitters" like the Chase Sapphire Reserve or the American Express Platinum and expect an approval, assuming your income supports it. These cards require "Excellent" credit, and 744 fits that bill. You'll get the big sign-up bonuses, the airport lounge access, and the high credit limits.

However, don't get cocky.

Applying for three cards in one month will tank that 744 faster than you can say "overdraft." Each hard inquiry is a tiny dent. Usually 5 to 10 points. If you drop from 744 to 729, you might actually fall out of that top-tier interest rate bracket for a mortgage. If you’re planning a big purchase in the next six months, put your credit card applications on ice. Seriously. Just wait.

The "Ghost" of Credit Past

Sometimes a 744 is a "recovered" score. Maybe you had a bankruptcy seven years ago or a collection account from a medical bill that finally aged off. If that's the case, your score is on a massive upward trajectory.

But keep in mind that some lenders, especially for high-level security clearances or certain financial jobs, look at the full report, not just the score. They see the "ghosts." A 744 with a clean history is slightly more powerful than a 744 with a murky past. It shouldn't stop you from getting a loan, but it might mean a human underwriter asks you a couple more questions during the process.

How to push a 744 into the 800s (if you really want to)

It's actually simpler than most "credit gurus" make it sound. It’s mostly about boredom and discipline.

First, check your utilization. If you're using more than 10% of your total available credit, pay it down before the "statement closing date," not the "due date." This is a pro tip. The score is calculated based on what the bank reports on the closing date. If you pay it on the due date, the high balance has already been reported to the bureaus.

Second, ask for limit increases. If you have a 744, your banks probably trust you. Call them up and ask to move your $5,000 limit to $10,000. Don't spend more. By increasing the limit, you automatically lower your utilization percentage. It’s a math hack.

Third, stop closing old accounts. That dusty old card from college that you never use? Keep it open. It's contributing to your "average age of accounts." Closing it is like deleting a chapter of your history.

Lastly, check for errors. The FTC has found that about 25% of consumers have errors on their credit reports. A single "late payment" that wasn't actually late can drag a potential 790 down to a 744. Use a service like AnnualCreditReport.com to see the actual data, not just the flashy number on your banking app.

Actionable steps for your 744 score

You’ve got a great score. Don’t stress it too much. But if you want to optimize your financial life, here is what you do next:

- Audit your utilization: Get your total balances under 10% of your total limits. This is the fastest way to see a jump.

- Verify your "Rate Shopping" window: If you are looking for a car or home, do all your applications within a 14-day window. The scoring models will treat multiple inquiries as a single event, protecting your score.

- Set up "Safety Net" autopay: Even if you like paying manually, set up a minimum payment autopay. One missed payment can tank a 744 by 60 to 100 points. It’s a long climb back up.

- Use your leverage: If you're applying for a loan, tell the loan officer you know your score is 744 and you expect the best tier. Sometimes they’ll try to "buffer" the rate—don't let them.

- Monitor the right things: Ignore the daily fluctuations of 2 or 3 points. It’s noise. Look at the 6-month trend.

A credit score of 744 is a badge of honor. It says you’re reliable, you understand how money works, and you aren't a risk. You aren't perfect, but in the eyes of the American financial system, you're pretty close to it. Use that leverage wisely, don't get greedy with new credit lines, and you'll find that doors start opening a lot easier than they used to.

Whether it's that 2% interest rate on a new SUV or a mortgage that doesn't make you wince every month, your 744 is doing the heavy lifting for you. Just keep doing what you're doing. It’s working.